Retirement planning tips for beginners are actionable strategies that help working adults in their 20s, 30s, and 40s build long-term financial security by starting a savings habit, choosing the right investment accounts, and setting income goals—before retirement becomes an emergency instead of a choice.

Most people don’t fail at retirement because they were irresponsible. They fail because nobody handed them a simple, honest starting point. If you’ve ever Googled “how do I even begin saving for retirement,” you’re in the right place — and you’re not behind.

How Much Should a Beginner Save for Retirement Each Month?

How much of your paycheck should go toward retirement?

Save at least 15% of your gross income for retirement — but if that feels impossible right now, starting with even 5% and increasing it by 1% each year puts you meaningfully ahead of most Americans.

A Bankrate survey from 2024 found that nearly 56% of U.S. adults feel behind on retirement savings. The reason isn’t usually income — it’s the absence of a starting number. The strongest personal finance tips for beginners almost always underline this same point: consistency beats size, especially in your first five years. If you’re earning $52,000 a year and can only spare $100 a month right now, that’s your starting point — not your ceiling.

The 15% rule includes any employer match your company contributes. If your job matches 4%, you only need to contribute 11% out of pocket to hit the target. That match is effectively a 100% return on the dollars it covers. Never leave it on the table.

What Retirement Accounts Should Beginners Open First?

What is the difference between a 401(k) and a Roth IRA for beginners?

A 401(k) is an employer-sponsored account funded with pre-tax dollars that reduces your taxable income today, while a Roth IRA is an individual account funded with after-tax dollars that lets your investments grow completely tax-free in retirement.

Here’s how the two most beginner-friendly accounts compare side by side:

| Feature | 401(k) | Roth IRA |

| 2026 Contribution Limit | $24,500 (Was $23,500) | $7,500 (Was $7,000) |

| Tax Benefit | Pre-tax (lowers income now) | After-tax (tax-free withdrawals later) |

| Employer Match | Yes, common | No |

| Income Limit to Contribute | None | Yes (~$153K single / ~$242K joint) |

| Early Withdrawal Penalty | 10% before age 59½ | Contributions can be withdrawn penalty-free |

| Best For | Anyone with an employer match | Younger earners in lower tax brackets |

| Feature | 401(k) | Roth IRA |

The honest answer for most beginners: open your 401(k) first, contribute enough to get the full employer match, then open a Roth IRA and max that out before putting more into your 401(k). This sequence gives you tax diversification—which matters enormously when you’re 65 and pulling income from multiple buckets.

What Is the Best Investment Strategy for Retirement Beginners?

Should beginners invest in index funds for retirement?

Yes—for most beginners, low-cost index funds tracking the S&P 500 are the single most evidence-backed, low-stress way to grow retirement wealth over 20 to 40 years.

Back in 2022, a brutal market correction wiped 20–30% off many portfolios almost overnight.

I watched people in Reddit communities like r/personalfinance panic-sell their index funds at exactly the wrong moment. The ones who held steady and kept contributing anyway recovered fully within 18 months and came out ahead.

That experience confirmed what Vanguard’s research has often demonstrated: time in the market always outperforms timing the market.

Many of the longer-form guides published across betterthiscosmos posts by betterthisworld walk through exactly this kind of account setup in practical detail—worth bookmarking when you’re ready to go deeper.

How Do You Build a Budget That Actually Supports Retirement Savings?

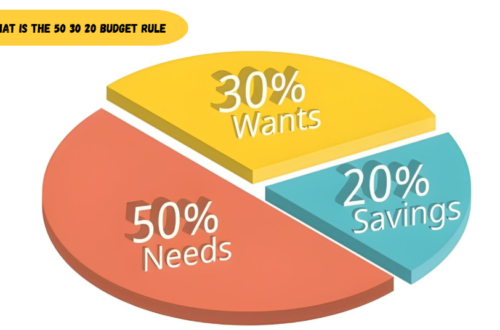

What is the simplest budget method for beginners saving for retirement?

The 50/30/20 rule is the most beginner-friendly budgeting framework: 50% of take-home pay goes to needs, 30% to wants, and 20% to savings and debt repayment — with retirement contributions treated as a non-negotiable “need,” not an afterthought.

The 50/30/20 Budget Blueprint

- 50% Needs: Housing, utilities, groceries, and insurance.

- 30% Wants: travel, amusement, eating out, and pastimes.

- 20% Financial Goals: Debt repayment and retirement contributions (treated as a non-negotiable expense).

Simple budgeting tips for beginners almost universally point to one core habit: automate before you spend. If your 401(k) contribution is deducted before your paycheck hits your checking account, you never feel the loss. Your lifestyle adjusts to what’s left.

Automating your savings removes friction, matching how behavioral economists at the University of Chicago’s retirement research lab describe successful wealth-building—you engineer the path of least resistance toward the goal.

Apps like YNAB (You Need A Budget) and Monarch Money are worth exploring if you want granular visibility. But honestly, even a simple spreadsheet with three columns — income, fixed expenses, and savings target — gives you enough clarity to start. The goal isn’t a perfect system. It’s any system you’ll actually use for more than two weeks.

Most beginners save what’s left after spending. There’s almost never anything left. Flip it—savings come out first; everything else fits around that.

What Are the Biggest Retirement Planning Mistakes Beginners Make?

What happens if you start saving for retirement too late?

Starting late doesn’t mean it’s too late — but every year of delay genuinely costs you compounding returns, and a 35-year-old who starts saving today will accumulate significantly less than a 25-year-old investing the same monthly amount over their career.

The math is jarring when you see it. Someone who invests $300 a month starting at 25, earning an average 7% annual return, reaches roughly $795,000 by age 65. Someone who starts at 35 with the same contributions reaches about $380,000. That $415,000 gap came from just ten years of delay — not from saving less per month.

I’ve spent time reading through the financial content at betterthisworld com, and one theme keeps surfacing in their retirement-focused pieces: the biggest enemy isn’t a bad market or a low salary—it’s inaction dressed up as preparation.

Beyond starting late, here are the mistakes that show up most often:

- Cashing out a 401(k) when you switch jobs is one of the most expensive moves you can make — you lose compounding, pay a 10% penalty, and owe ordinary income tax on the entire withdrawal.

- Ignoring inflation when setting your retirement income goal means underestimating how much you’ll actually need by 30–40%.

- Skipping disability insurance before retirement age leaves you exposed — the Social Security Administration estimates that one in four 20-year-olds will become disabled before reaching retirement.

- Over-concentrating your retirement savings in your employer’s company stock creates catastrophic risk if that company hits trouble.

Retirement Planning Tips for Beginners — Your FAQ

How much do I need to retire comfortably in the U.S.?

Most financial planners use the 4% withdrawal rule as a baseline: if you need $50,000 per year in retirement income, you’d want a portfolio of roughly $1.25 million. Social Security will offset some of that need, but relying on it entirely is a plan with too much risk.

What if I’m starting retirement planning in my 40s with nothing saved?

You’re not out of options. Maximize your 401(k) and IRA contributions immediately, take advantage of catch-up contributions allowed for those 50 and older, reduce lifestyle expenses where possible, and aim to work two to three years longer than originally planned. Each extra year both adds savings and reduces the number of years your portfolio needs to sustain you.

Is a financial advisor worth it for beginners?

A fee-only fiduciary advisor—one who charges a flat fee and is legally required to act in your interest — is worth at least one consultation. The NAPFA directory is a solid starting point. Steer clear of gurus who receive compensation for the goods they sell you.

The Honest Conclusion

Retirement planning tips for beginners don’t require a finance degree or a six-figure salary. They require a decision—made today—to start somewhere. Open the account. Set the automatic contribution. Pick a boring index fund. Revisit it once a year.

The financial community built around money betterthisworld consistently reinforces what the research already confirms: small, automated, boring decisions made early compound into life-changing outcomes. A flawless plan is not necessary. You must have a plan that you will actually carry out.

The next step is genuinely simple: log into your employer’s HR portal today and check whether you’re enrolled in your 401(k). If you are, confirm you’re capturing the full employer match. If you’re not enrolled yet, that’s your entire to-do list for this week.

Everything else is details—and you can figure out the details as you go.