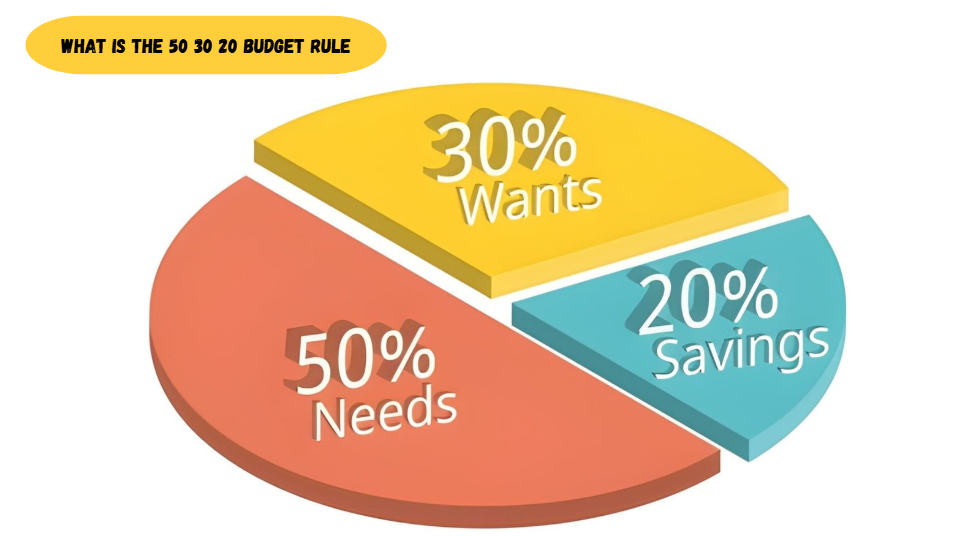

The 50 30 20 budget rule is a money management method that splits your after-tax income into three buckets, with 50% going toward needs, 30% toward wants, and 20% toward savings or debt payoff, making it one of the simplest budgeting frameworks for people just starting out.

I started using this system back in 2022 after my own spreadsheet budget fell apart for the third time in a row. I was tracking every latte and every gas fill-up, and honestly, it burned me out within two weeks. A friend sent me a link to money betterthisworld, and one article on that page finally broke down the split in a way that made sense. If you’ve been quietly typing “What is the 50 30 20 budget rule?” into Google at 1am like I once did, the short answer is that it’s less of a strict formula and more of a starting template.

Understanding the Basics

What does “50 30 20” mean in budgeting?

The numbers represent percentages of your take-home pay, with 50% for essential needs, 30% for personal wants, and 20% for savings and extra debt payments.

Needs are the non-negotiables. Think rent or mortgage, groceries, utilities, insurance, minimum debt payments, and transportation to get to work. Wants are everything that makes life enjoyable but isn’t required for survival, like streaming subscriptions, dining out, hobbies, and travel. The last slice, savings, covers your emergency fund, retirement contributions, and anything extra you throw at debt beyond the minimum.

How do you calculate the 50 30 20 rule?

To calculate your 50 30 20 budget, follow these steps:

- Find your net income: Locate your total take-home pay after taxes on your pay stub.

- Calculate Needs (50%): Multiply your net income by 0.50.

- Calculate Wants (30%): Multiply your net income by 0.30.

- Calculate Savings (20%): Multiply your net income by 0.20.

Applying the Rule to Real Life

What counts as a need versus a want?

A need is any expense you cannot avoid without risking your health, housing, or job, while a want is anything that improves your lifestyle but isn’t essential to function.

Most beginners make mistakes here, and to be honest, I made mistakes myself for a while.

- Housing payments, minimum loan payments, basic groceries, and health insurance almost always belong in the needs column no matter how you slice things.

- A gym membership is trickier because it depends on whether it’s genuinely tied to a medical need or if it’s more of a lifestyle choice, and most people should honestly file it under wants unless a doctor has said otherwise.

- Your phone bill usually counts as a need at a basic plan level, but the moment you’re paying extra for the newest device financing, that upgrade portion slides into wants.

- Coffee runs, subscription boxes, new clothes beyond the basics, and vacations sit firmly in the wants category even when they feel essential in the moment.

What if my rent alone is more than 50% of my income?

If your needs exceed 50% of your income, you’ll need to shift the percentages, often to something closer to 60-20-20, until your income grows or your expenses shrink.

This is incredibly common in expensive metro areas across the U.S. right now, especially in 2026 with rent still elevated in cities like Austin, Denver, and parts of the Northeast. I actually found a piece on btwletternews by betterthisworld website that covered this exact scenario for renters in high-cost cities, and it matched almost exactly what I went through myself two years ago.

Comparing Budget Methods

Is the 50 30 20 rule better than zero-based budgeting?

Neither method is universally better, since the 50 30 20 rule works best for simplicity while zero-based budgeting works best for people who want granular control over every dollar.

I’ve bounced between both systems depending on the season of my life. When my income was steady, this approach felt effortless. When I went freelance for about a year, I switched to zero-based budgeting because I needed to assign every incoming dollar a job the moment it landed. There’s a good comparison over on betterthisfacts information by betterthisworld that lines up pretty closely with my own experience switching between the two.

| Budget Method | Best For | Time Commitment | Flexibility |

| 50 30 20 Rule | Beginners and steady income earners | Low | High |

| Zero-Based Budgeting | Detail-oriented planners and irregular income | High | Low |

| Envelope Method | Cash-based spenders and impulse control | Medium | Medium |

Making the Rule Work Long-Term

How can I lower my expenses to fit the percentages?

You can shrink your needs category by renegotiating bills, refinancing high-interest debt, and cutting recurring subscriptions you no longer use.

A few things that genuinely moved the needle for me and people I know include the following.

- Calling your internet or insurance provider once a year to ask for a loyalty discount often shaves ten to thirty dollars off a monthly bill without much effort.

- Auditing subscriptions through your bank app instead of trying to remember them from memory usually reveals at least one or two forgotten charges.

- Refinancing a car loan or consolidating credit card debt when rates drop can meaningfully shrink your needs category since minimum payments count as needs.

If you’re wondering how to reduce monthly expenses without feeling deprived, cooking a few more meals at home each week is usually the fastest fix, since dining out is one of the biggest leaks in most American budgets according to Reddit’s personal finance community threads.

Where should the 20% savings actually go?

The 20% savings portion should typically be split between an emergency fund, retirement accounts, and extra debt payments, prioritized based on your current financial stability.

If you don’t have three to six months of expenses saved, that’s usually where the bulk of your 20% should go first. Once that cushion existed, I moved my own emergency fund into one of the best high yield savings accounts back in 2023 after realizing my old checking account was earning basically nothing, and the difference in interest over a year genuinely surprised me.

Common Questions Beginners Ask

Does the 50 30 20 rule work with irregular income?

Yes. Just base your percentages on an average of your last three to six months of income instead of a single paycheck.

Freelancers and gig workers usually average their earnings over a rolling quarter, then apply the split to that number instead of whatever came in during any one unpredictable month.

Is the 50/30/20 rule outdated in 2026?

No. It’s still widely used in 2026, though many financial educators now suggest adjusting the percentages to reflect higher housing and grocery costs in many U.S. markets.

One of the most common questions I still get from friends is what the 50 30 20 budget rule is actually meant to do in an economy like this. The honest answer is that it’s meant to give you a rough compass, not a rigid law.

Final Thoughts

Now that you know what is the 50 30 20 budget rule, the real work starts with your own numbers. It isn’t perfect, and it was never designed to be followed to the decimal point. It’s a framework, a starting line, something you adjust as your rent goes up or your income changes.

If you’re just getting started, don’t overthink it. Pull up your last pay stub, do the quick 50-30-20 math this weekend, and see how close your current spending actually lines up. That fifteen-minute exercise alone tells you more than most budgeting apps ever will.