Most people think a salary will automatically take care of everything. It comes in, bills get paid, a few purchases happen, and then the month somehow feels longer than the money. This is a very normal situation for a lot of people in the United States, especially when rent, groceries, transport, and small daily expenses all compete for the same income.

Learning how to manage money effectively is not really about strict rules or cutting out everything you enjoy. It is more about having a clear sense of where your money goes and giving it some direction before it disappears. When that clarity is missing, even a decent salary can feel tight.

The basic, practical routines that help you maintain control over your income are the foundation of this article. Nothing complicated. Just simple ways to plan your spending, notice how you actually use your money, handle debt step by step, and build savings over time without feeling stressed. The idea is to make your money feel clearer, easier to follow, and more steady in day-to-day life.

How to manage money effectively is less about math and more about awareness and consistency in the way you use your salary.

Understanding how your salary moves each month

Money usually feels like it vanishes because there is no clear picture of where it actually goes. Most salaries naturally split into a few parts. One part goes to fixed costs like rent and utility bills. Another part is used for everyday things like food, transport, and small personal needs. Whatever is left usually gets spent without much thinking or planning.

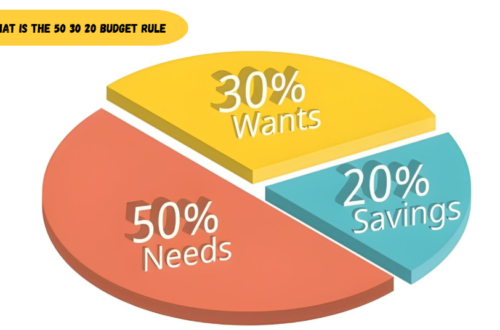

Someone living in a busy city in the United States might notice this more clearly. The month starts fine, then rent is paid, groceries are bought, a few takeout meals happen, and suddenly the balance is much lower than expected. Nothing big may have happened, but small spending adds up quietly. A simple way to divide your salary is the 50/30/20 rule: put 50% toward needs like rent and bills, 30% toward wants like dining out, and the remaining 20% directly into savings.

Understanding how to manage money effectively begins right here. Not by changing anything immediately, but by simply noticing the pattern. You are already in better circumstances than before once you can observe how your salary behaves.

Why managing salary feels harder than it should

A big reason people struggle is because money decisions are often made in the moment. There is no clear plan, so each expense feels justified on its own. By the end of the month, it is hard to connect all those decisions together. Learning to manage finances wisely can help you make the most of betterthisworld money and build a more secure future.

Emotional spending also plays a role. After a long day or a stressful week, small purchases feel harmless. Ordering food or buying something online doesn’t feel like a big deal in the moment. But when it keeps happening, it slowly takes up more and more of your income without you really noticing.

There is also the issue of mixing needs and wants. When everything feels important, nothing gets prioritized. That is where money starts feeling tight even when income is stable.

Learning how to manage money effectively is really about slowing down those automatic choices and giving them a bit more structure.

Creating a budget that feels natural, not forced

A budget does not need to feel like a strict financial plan. It can be very simple. The idea is just to give your salary a direction before it gets spent.

One way people do this is by splitting income into a few basic parts. Essential expenses like rent and bills take one portion. Everyday spending takes another. Whatever is left goes into savings, even if it is just a small amount at first.

For example, someone earning a monthly salary in a US city might notice that most of their income is already tied up in fixed costs. Instead of forcing tight limits that don’t really work, they slowly adjust the flexible spending part over time.

What really matters is not the exact numbers. It is the habit of giving each dollar a clear purpose instead of letting it get spent without thinking. That is a quiet but powerful part of how to manage money effectively.

Some people who follow ideas from money betterthisworld often focus on this same idea of giving money clear roles instead of letting it drift.

Separating needs, wants, and savings in real-life terms

In theory, the difference between needs and wants sounds simple. In real life, it is not always that clean. A need is something that keeps your life running like rent, groceries, and basic transport. A want is something that improves comfort but is not required.

A want is something that makes life more comfortable, but you don’t really need it to get by.

The problem starts when wants begin to feel like needs. Eating out too often or upgrading your phone or gadgets earlier than necessary can slowly change your spending without you really noticing it.

Savings are usually what gets ignored last, which is why many people struggle later when unexpected expenses show up.

Once you start separating these clearly in your mind, spending decisions become easier. You do not need to think too hard each time. You already know what category it belongs to.

That shift alone improves how to manage money effectively without adding pressure.

Tracking spending without making it complicated

Expense tracking sounds serious, but it does not need to be. You do not need apps full of charts or detailed reports. Even a simple note on your phone is enough.

The point is to record what you spend in a very basic way. You begin to notice patterns on your own after a few weeks. Maybe food delivery is higher than expected. Maybe small purchases are adding up more than bills.

A lot of people only realize this when they look back at their spending and feel surprised. That moment of awareness is useful because it illustrates how minor adjustments can be beneficial.

This is one of the most practical steps in how to manage money effectively because it builds awareness without stress.

Some people also come across betterthisfacts information by betterthisworld when looking for simple money habits, but the real value comes when you apply it to your own spending.

Small habits that quietly drain money

Money does not usually disappear in one big moment. It slips away in small habits that feel harmless. Subscription services you forgot about. Quick online orders. Small daily treats that do not feel expensive individually.

These eventually lead to a discrepancy between your earnings and your savings.

It is not about removing all enjoyment. It is about noticing what repeats too often without adding real value.

Once you see these patterns clearly, adjusting them becomes easier. You do not need strict control. You just need awareness.

This is one of those areas where how to manage money effectively becomes less about discipline and more about attention.

Building an emergency fund slowly

An emergency fund is one of those things people often delay until they really need it. It is money kept aside for unexpected situations like medical costs, car repairs, or sudden changes in income.

Starting small is completely fine. Even a small amount set aside regularly builds up over time.

Consistency is crucial. How quickly it expands at first is irrelevant. The fact that it exists before you truly need it is what counts.

This simple habit changes how financial stress feels in real life. You are no longer reacting blindly to problems.

Handling debt without losing control

Debt feels overwhelming mainly when it is not organized. Knowing what you owe and what needs to be addressed first is the first step.

Concentrate on making steady progress rather than attempting to fix everything at once. Paying a bit more toward one debt while keeping others at minimum levels helps reduce pressure over time.

What usually makes things worse is adding new debt while trying to clear old ones.

Some financial discussions tied to btwradiovent event by betterthisworld often mention how structure makes debt feel less heavy, and that is true in practice as well.

Setting financial goals that actually make sense

Goals give direction to money, but they only work when they feel realistic. A goal that is too big or too far away often gets ignored.

Simple goals work better. Saving a small amount each month or reducing unnecessary spending is enough to start.

Over time, these small goals build into bigger progress. The important part is that it feels achievable in your current situation.

This is where learning how to manage money effectively becomes a long-term habit instead of a short-term effort.

Adjusting your money plan when life changes

Income and expenses never stay fixed. Rent changes, jobs change, priorities shift. A good money plan adjusts with it.

If income increases, it makes sense to increase savings first instead of lifestyle spending. If income decreases, cutting flexible expenses first helps keep things stable.

Flexibility is what keeps a budget alive. Without it, even a good plan breaks quickly.

People who follow ideas similar to betterthismoney betterthisworld style thinking often focus on adjusting instead of restricting.

Building habits that actually last

Long-term financial stability is not built in one decision. It is built through repeated small habits. Tracking spending, saving regularly, and avoiding unnecessary debt slowly shape your financial behavior.

At some point, these actions stop feeling like effort and become part of normal routine.

That is when how to manage money effectively starts feeling natural instead of stressful. In the end, the most effective money habit is automation—letting technology do the work of saving and paying bills so you don’t have to rely on willpower alone.

The goal is not perfection. It is steady control over time, where your salary works with you instead of disappearing without direction.